The BYDFi crypto exchange offers an exclusive rewards and bonus programme where you can unlock significant benefits by completing simple tasks such as signing up…

Financial Tools Discounts Category

In this section you can find great discounts, offers and promo codes that will allow you to save money on the best online financial tools. From stock screeners, trading platforms, fintech apps,... to discount coupons from the best prop firm brands and online brokers.

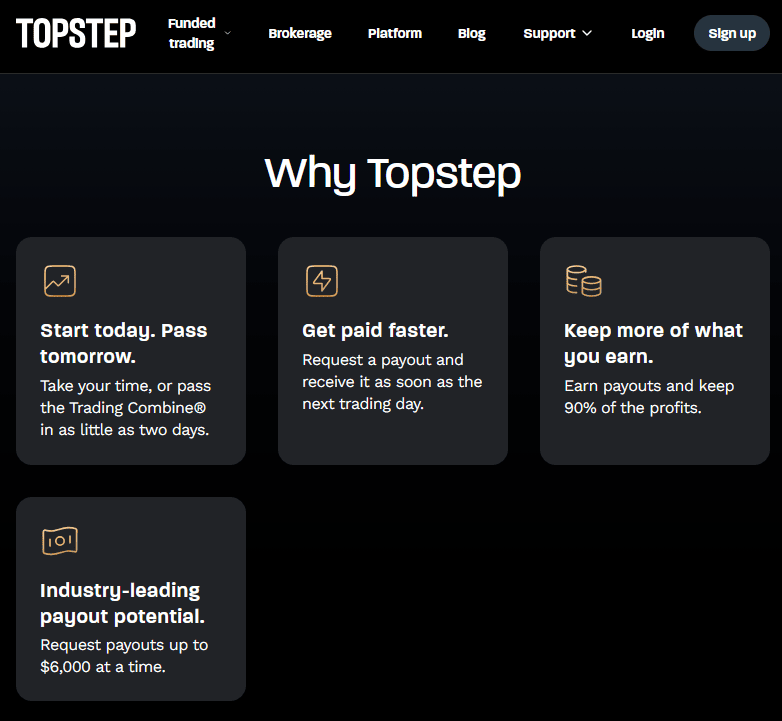

Topstep 30% Off Promo Code in July 2026

Topstep has recently launched an exclusive official deal with a promo code that lets you save 30% on up to 5 evaluation accounts (Trading Combine)…

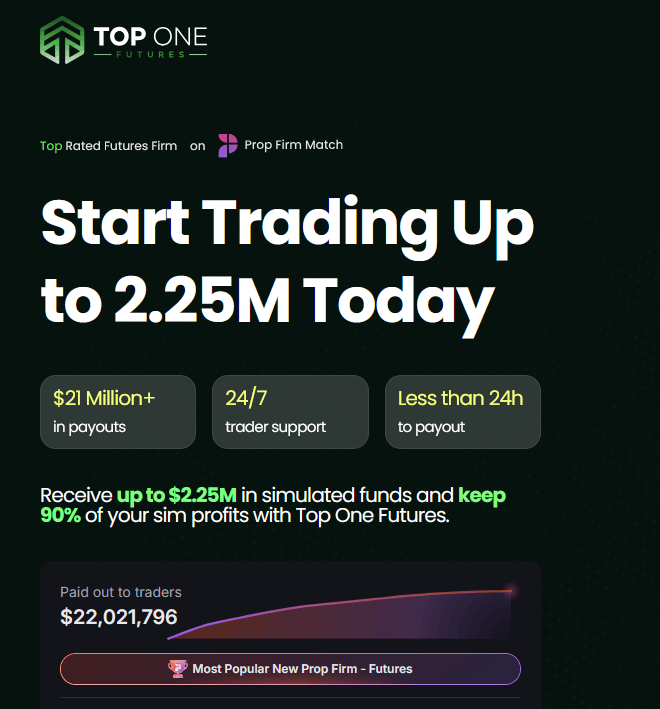

Top One Futures 60% Off Coupon Code in July 2026

Top One Futures offers a coupon code that gives you a 60% discount on your first purchase of any funded account. If you were looking…

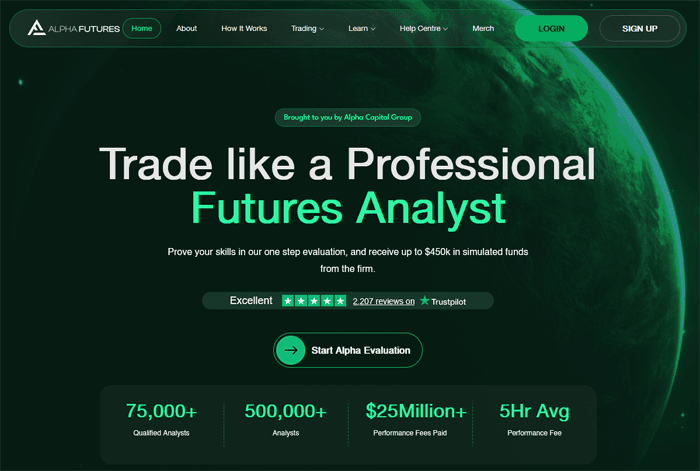

Alpha Futures 25% Off Discount Code (July 2026) – Verified

Alpha Futures offers an exclusive discount code valid for any evaluation account that will allow you to save a significant amount of money. With this…

ThePropTrade 10% Off Coupon Code

ThePropTrade offers an exclusive coupon code to save on your evaluation and accelerate access to funded capital. With this thePropTrade promo code , you activate…

OneUp Trader Up To 30% Off Promo Code

OneUp Trader offers an exclusive promo code that gives you up to 30% off any funded account. The percentage is adjusted to the company’s current…

Blue Guardian Up To 50% Off Coupon Code

Blue Guardian offers a coupon code that allows you to save 50% on your first purchase of any funded account on any of the models…

Prop Firms Discount Codes And Coupons (July 2026) – Verified

Get verified promo codes for the top prop trading firms in one place. We check the official channels of major brands, newsletters, specialised websites and…

Funding Pips 20% Off Discount Code in July 2026

Funding Pips offers an exclusive coupon code that gives you 20% off the price of access to any of its funded accounts for trading. If…

My Funded Futures Up to 50% Off Discount Code (July 2026) – Verified

My Funded Futures currently offers a discount code that allows you to get up to 50% off any of its funded accounts. If you are…

Bookmap Up to 50% Off Coupon Code in July 2026

Bookmap is a trading platform designed for traders and investors seeking a competitive edge in financial markets. It uses an innovative heatmap to display order…

Cryptohopper Up to 47% Off Discount Code

Want to maximize your cryptocurrency trading profits while saving on your subscriptions? Cryptohopper is currently offering a discount code that allows you to save up…

FXIFY 26% Off Discount Code in July 2026

FXIFY offers an incredible discount through a coupon code that gives you 26% off on any funded account, whether it’s a 1-step, 2-step, or 3-step…

Apex Trader Funding 90% Off Coupon Code in July 2026

Apex Trader Funding, the popular futures prop firm, is currently offering an exclusive coupon code with which you can save a good amount of money…

BluSky 30% Off Coupon Code

BluSky Trading offers a coupon code with which you can save 30% off the price of any of their evaluation plans. Founded in 2022 and…

Elite Trader Funding Up to 80% Promo Code – July 2026 Verified

Currently, Elite Trader Funding is offering a 80% off promo code on one of their most popular evaluations or up to 50% discount on other…

Funded Trading Plus 10% Off Discount Code

Funded Trading Plus is now offering a 10% discount by using a special coupon code—which we’ll provide at no cost. All new users who purchase…

Token Metrics 26% Off Coupon Code

Token Metrics is an online tool designed to help cryptocurrency investors and enthusiasts make informed decisions using artificial intelligence and data analysis. For your convenience,…

Benzinga Pro Up to 41% Off Promo Code

Benzinga Pro offers a promo code that allows you to save up to 41% on the price of your Essential plan. With this discount coupon,…

Take Profit Trader 40% Off Promo Code (Verified in July 2026)

Currently, Take Profit Trader offers a promo code that gives you 40% discount (and never pay an activation fee) when purchasing one of their available…

Trade Ideas 45% Off Promo Code – July 2026 Verified

Trade Ideas is currently offering a promo code that will allow you to get up to 45% discount on any of its subscription plans (Trade…