Table of Contents

What Is a Break-Even Price?

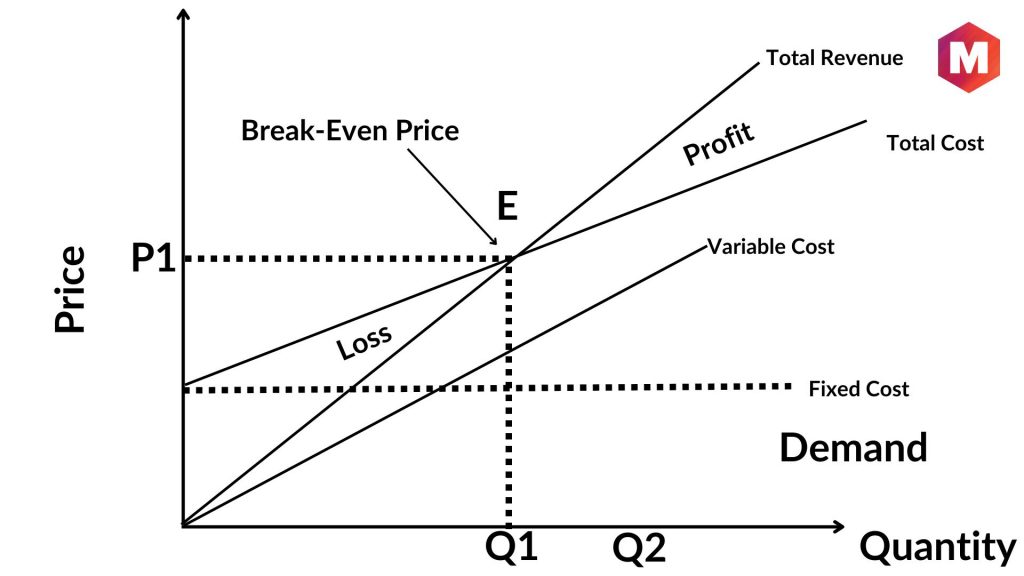

The break-even price is the price a company must charge to cover direct manufacturing expenses and make a profit. It occurs when sales revenue equals variable production expenses.

Companies can profitably sell products or services above break-even. If the price falls below break-even, the company loses money on each sale and may fail if it sells too cheaply for too long.

Break-even pricing is a market penetration strategy that sets the product’s price so the company never profits or loses money.

The break-even price has a simple pricing methodology.

Total cost / breakeven price = fixed + variable.

Thus, determining fixed and variable expenses is essential to break-even pricing, which is used when entering new markets and building business and marketing strategies.

Key Takeaways:

- The break-even price is the amount a company must charge for its product/service to cover all production expenses and achieve the desired profit margin. It is the moment when total revenue equals all variable production expenses. Above this price, a company profits; below it, it loses.

- The break-even price approach involves entering a market by pricing the goods so that the company makes neither a profit nor a loss. This method is commonly used when entering a new market or developing business and marketing initiatives.

- The break-even price is mostly determined by an organization’s fixed and variable costs. These costs must be correctly identified and controlled to sustain this pricing strategy. The break-even price is calculated using the formula: fixed cost + variable cost = total cost/break-even price.

Break-Even Price Formula

The break-even price is a concept used to determine the sales volume that would allow a business to cover its costs. When you set your break-even price, you’re trying to figure out how many products or services you’d have to sell to take back the money you spent on creating them.

The formula for calculating the break-even price is:

Break-even point = fixed costs/unit variable cost

Break-even points can vary by industry and product, but they’re usually calculated based on fixed costs, all the expenses you must pay regardless of how many units you sell—things like rent and insurance. Variable costs, such as packaging materials and shipping fees, vary with each unit sold.

Break-Even Price Strategy

When you start a business from an idea, you want it to be successful and sustainable. However, building revenues takes time for every startup. In these circumstances, a lower break-even point is appropriate when you are neither profitable nor losing. Profit is the ideal goal; however, breaking even is another option.

The break-even price is when a product, service, or asset must be sold to cover its manufacturing or provision costs. The break-even price is used to enter new markets with low prices and steal clients from competitors. It could work if the company has the resources to increase production volumes until it reduces costs and profits at the break-even price. Thus, the Break-even price seeks scale economies.

Although it seems like a good concept, this technique has risks that, if not managed properly, could put your organization at risk. The break-even price can be an entry barrier, market dominance tool, and competition reduction instrument. Break-even price strategies discourage new market entrants since profits are low.

Market dominance is achieved by growing production capabilities and realizing economies of scale.

Fixed and Variable Costs in Break-Even Pricing Strategy

Businesses must be able to identify their fixed and variable costs before setting a break-even point. Fixed costs do not change over time, no matter how many units are produced or sold. Examples include rent and insurance premiums. Variable costs fluctuate depending on production levels and are directly related to unit sales volume. These include raw materials, labor costs, and advertising expenses.

Once a company has identified its variable and fixed costs, it can use these figures and its revenue projections to find its break-even point—the price at which it can sell enough units to cover its variable and fixed costs without any losses.

Relevance And Uses of Break-Even Formula

The Break-Even Formula is essential in management and cost accounting. It helps organizations demonstrate financial savvy and make strategic decisions for profit by navigating the many factors and statistics they face.

Here are some key break-even formula applications and benefits:

- Profitability Assessment: The break-even calculation helps businesses and new initiatives assess profitability. This crucial unit of analysis determines the sales needed to meet operational costs and profit.

- Data-driven Pricing: The break-even method helps businesses find the best pricing model for profitability by comparing price levels and cost structures. This is very useful for pricing new products or services.

- Project Management Tool: The break-even formula is essential for project management. It determines the best price levels to maximize profit and minimize project risk.

- Sales Planning and Marketing Strategy: The break-even formula links cost analysis, price, and marketing. By knowing the break-even point, marketers can build numerical tactics to reach the required sales, which can affect marketing campaigns.

- Competitive Dynamics: A rigorous break-even study shapes competition. It raises the entrance hurdle for new vendors by defining expenses vs sales. Businesses that perform a thorough break-even analysis may change their operating strategies, challenging competition.

Examples of Break-Even Points

You’ve just started a business selling makeup. You have $300,000 in start-up costs and make $250,000 worth of yearly sales. Your cost of goods sold is $150,000, so you need to bring in $200,000 in revenue to cover those costs and make a profit.

But what if you want to know how much money you need to charge customers for each product to reach your company’s break-even point? You might try calculating how much money it takes to cover your fixed expenses—your rent/mortgage payment and other overhead—but this approach would give you an inaccurate answer because it would include the variable cost associated with each sale.

Instead, try using break-even analysis. This lets you determine how many units must be sold for your business to be profitable (i.e., not lose money).

For example, a company that sells widgets has $100,000 in fixed costs per year. Each widget sells for $10 and has a variable cost of $5 per unit. The company’s contribution margin per unit is, therefore $5 ($10 minus $5).

To find the break-even sales price, divide $100,000 by $5: 100,000 / 5 = 20,000 units. The company must sell 20,000 widgets yearly to break even; any fewer than that and it loses money; any more than that, and it makes a profit.

Positive Effects of Break-Even Prices

The break-even price is a method used in accounting to calculate the price at which a product will generate no profit. Break-even prices can give businesses the confidence to set high enough to create a profit yet low enough to remain competitive and attract customers. They can also help companies to plan for their future.

Setting the prices at break-even increases market share, drives away existing competitors, and creates an entry barrier for new competitors. By limiting competition, this ultimately results in a dominant market position.

Negative Effects of Break-Even Prices

But let’s take a look at the drawbacks now. We have been discussing penetration pricing in a previous article. Something similar can also happen by using the break-even price. Once you present the market with a really low cost compared with your competitors, it is hard to increase prices afterward. Improving the quality of the offered product or service might be possible. Once you enter the market at a low price, you might risk losing your customers when prices are raised.

On the other hand, if you have been in the market for a period and suddenly reduce pricing to increase your market share, then a perception problem will appear, as customers might doubt the quality of the provided product, considering that there might be a quality issue because of the lowered prices.

Moreover, a price war can be declared. Some of your competitors might decide to play the same game as you, so you will not earn any market share. Lastly, the most dangerous situation can be that you decide to penetrate with break-even pricing. Still, the cost was not calculated correctly, or you cannot sustain the break-even price, in which case you will have to exit with heavy losses.

Conclusion!

By knowing the total fixed costs, the volume of the production, and the variable costs per unit, the company can calculate the break-even price. It should be considered that the total amount counted as fixed costs will remain constant, unlike the variable costs, which will differ according to the production. Thus, economies of scale will be the target here, as more production units will mean lower fixed costs and controlled variable costs per unit.

FAQs

1) How Can I Use Break-Even Prices?

The break-even price is the amount that covers the cost or investment of a product or service. For example, selling your land for the same price you bought it won’t profit or suffer losses. Although the calculation of the break-even price may differ depending on the industry or situation, its basic definition remains unchanged.

2) What Benefits Do I Get From Using Break-Even Prices?

The most significant benefit of using the break-even pricing strategy is that it helps companies reduce the risk of losses and make profits more predictably. Through this strategy, companies can keep their business afloat even when market conditions are not favorable. Break-even pricing can establish a trustworthy brand image by demonstrating that you are providing a product or service at a competitive price.

3) What Is the Break-even Price for an Options Contract?

The break-even price of an options contract can be defined as the sum of the strike price and the option’s premium. Let us take a simple example to demonstrate this: Consider a call option with a strike price of $30 and a premium charge of $3. The break-even price will be $33.

In contrast, in comparable circumstances, the calculation for a put option favors subtraction over addition. Assuming a put option with the same strike price and premium cost as above, which are $30 and $3, respectively, the break-even price is $27.

In summary, the break-even price is critical for investors to make informed judgments about buying or selling options.

4) Why Should Taxes and Fees Be Included in a Break-Even Analysis?

Breaking even is crucial for any business and investment. When costs equal revenue, a business is neither profitable nor losing. Break-even analysis must include taxes and fees, even though many see this point from a gross profit viewpoint. They are prevailing costs, so removing them may skew the break-even point and misrepresent corporate financial health.

Taxes apply to stock sales and other company activity. Consider a $10 stock sale profit taxable under long-term capital gains. At 15%, you owe $1.50 in taxes. Without this tax, you may exaggerate profits by $1.50.

Additionally, commission fees might greatly affect break-even. For example, a stock trade with a $1 commission fee raises the break-even point.

Estimating business operations and making strategic decisions, including such expenses, when estimating your break-even point. By considering taxes, fees, and inflation, you can determine when break-even happens and account for all the real-world elements affecting your organization.

Liked this post? Check out the complete series on Marketing