Let’s explore the detailed SWOT Analysis of Bank of Baroda by understanding its strengths, weaknesses, opportunities, and threats.

As one of India’s top public sector banks, Bank of Baroda combines tradition and innovation. Since 1908, it has built a global branch network to provide retail and corporate banking services. Its strategic mergers and digital innovation emphasize accessibility and client pleasure.

Bank of Baroda is an example of trust and durability in global finance. The bank’s broad portfolio and technology enable it to meet varied consumer needs. Sustainable growth and operational excellence boost its market position and attract many clients as it moves forward.

Overview of Bank Of Baroda

- Industry: Banking, Financial services

- Predecessor: Vijaya Bank, Dena Bank

- Founded: 20 July 1908, 115 years ago

- Founder: Sayajirao Gaekwad III

- Headquarters: Vadodara, Gujarat, India

- Number of locations: 8243 Branches, 10,033+ ATMs (March 2023)

- Area served: India & Worldwide

- Key people: Hasmukh Adhia (Chairman), Debadatta Chand (MD & CEO)

- Revenue: Rs 1.42 lakh crore (US$17 billion) (2024)

- Operating income: Rs 25,799 crore (US$3.1 billion) (2024)

- Net income: Rs 18,767 crore (US$2.2 billion) (2024)

- Total assets: Rs 16.55 lakh crore (US$200 billion) (2024)

- Total equity: Rs 1.18 lakh crore (US$14 billion) (2024)

- Owner: Government of India (63.97%)

- Number of employees: 79,806 (2022)

- Website: www.bankofbaroda.in

Table of Contents

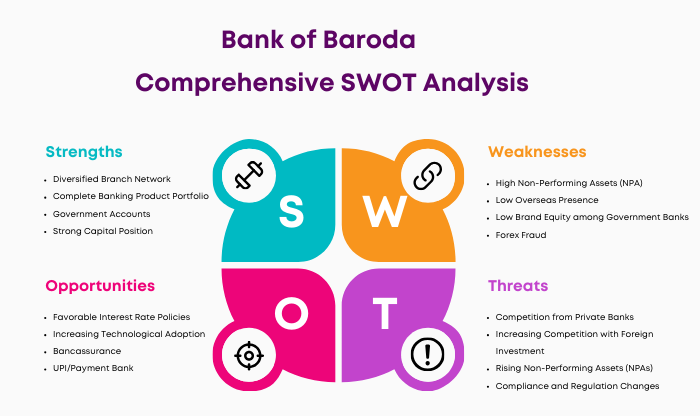

SWOT Analysis of Bank of Baroda

Strengths of Bank of Baroda

1. Diversified Branch Network

Bank of Baroda, India’s second-largest bank, is known for its size and vast reach. As of March 2024, the bank has about 8,243 branches nationwide in 17 countries. The Bank has a significant international presence with 91 overseas branches/ offices spanning 17 countries (including overseas subsidiary operations). This extensive network encourages resources at a lesser cost, allowing the bank to supply financial services nationwide efficiently.

2. Complete Banking Product Portfolio

Bank of Baroda offers a wide range of financial services and products, living up to its name. This complete portfolio meets all of its clients’ financial needs in one place, making it a one-stop shop for financial services.

3. Government Accounts

Bank of Baroda manages several government accounts and is trusted by the government. The bank distributes pensions to railway pensioners and others. Certain government positions require government banks to process pay and pensions. This criteria gives the Bank of Baroda a stable and loyal customer base over commercial banks.

4. Strong Capital Position

Bank of Baroda has a strong financial position with a 37.81% capital adequacy ratio (CAR) as of March 31, 2023. As of the end of March 24, BOB’s total deposits reached Rs 13,26,919 crore. Of this amount, Rs 11,28,523 crore was in local deposits, and Rs 1,98,396 crore was in deposits outside Bhutan.

Total advances made worldwide were Rs. 10,89,822 crore, with Rs. 8,97,366 crore in advances made in India and Rs. 1,92,456 crore in other countries (Provisional).

5. Second Largest Bank

Bank of Baroda is India’s second-largest bank, with a market cap of $17.12 Billion as of June 2024. This status shows the bank’s financial strength and the trust of its broad customers.

6. Large Customer Base

The Bank serves its global customer base of ~165 million through over 70,000 touchpoints spread across 17 countries on five continents as of March 2023.

7. Merger Synergies

The Government of India merged the Bank of Baroda with Vijaya Bank and Dena Bank, creating the third-largest lender in India. This combination maximizes synergies, operational efficiency, bank reach, and client base.

8. Competitive Interest Rates

Bank of Baroda gives significantly cheaper rates than private sector banks. This competitive edge draws many people looking for affordable banking services.

9. Established Brand

Bank of Baroda is a renowned banking brand with a century-old history of trust and excellence. Due to its long history, the bank has a reputation for reliability, which generations have trusted.

10. International Presence

Bank of Baroda operates in different nations. The Bank has a significant international presence with 91 overseas branches/ offices spanning 17 countries (including overseas subsidiary operations). This cross-border expansion has diversified the bank’s customer base and allowed it to capitalize on global market opportunities.

11. Digital Advancements

Bank of Baroda promotes technological innovation that aligns with the digital revolution. The bank offers many online banking options to meet tech-savvy customers’ needs. The Bank of Baroda’s app is called ‘BoB World.’ Bob World app is called ‘BoB World.’ Bob World app has 8.1 million daily transactions.

12. Robust Training Infrastructure

Bank of Baroda invests in its human resources by providing training opportunities to keep its workers up-to-date on banking operations and customer service excellence.

13. Experienced Management

A team of experienced leaders and management professionals leads the bank toward continued growth. They guide the bank to operational excellence with their banking industry expertise.

14. CSR Initiatives

Bank of Baroda’s CSR efforts have improved its brand image. Community support for the bank’s activities strengthens its social responsibility.

15. Innovation

Bank of Baroda consistently launches new financial services and products to meet consumer needs and remain ahead of industry trends.

16. Loyalty Programs

The bank prioritizes customer retention through its loyalty programs. These promotions stimulate repeat business and increase cross-selling.

17. Risk Management

Bank of Baroda prioritizes a strict structure to protect its assets. This framework protects the bank from losses and strengthens its finances.

18. Financial Inclusion

Bank of Baroda is at the forefront of promoting banking accessibility for everybody. It helps bring unbanked and underbanked people into the financial mainstream, especially in rural and semi-urban areas.

Weaknesses of the Bank of Baroda

1. High Non-Performing Assets (NPA)

Bank of Baroda’s NPAs are expanding faster than its advances, which is concerning. This suggests that the bank needs help managing its loan portfolio, which could hurt its finances and future growth.

2. Low Overseas Presence

Bank of Baroda, one of Asia’s top 25 banks, generates the majority of its revenue from India. BOB is more vulnerable to domestic market fluctuations and less exposed to global and economic growth potential than Asia’s major banks due to its concentration.

3. Low Brand Equity among Government Banks

Bank of Baroda has struggled to create brand equity. Budget constraints limit the bank’s marketing efforts, resulting in less frequent and effective advertising than commercial banks. Consumer brand recognition and preference have decreased, especially compared to state-owned competitors like the State Bank of India.

4. Forex Fraud

The Reserve Bank of India sanctioned the Bank of Baroda for a nearly 6000-crore forex scam. Such accidents damage the bank’s economic survival and brand by diminishing customer and investor trust.

5. Integration challenges

The bank’s merger with Vijaya Bank and Dena Bank caused cultural, operational, and structural integration challenges. These issues might cause bank inefficiency and lower client satisfaction.

6. Operational Efficiency

Bank of Baroda loses efficiency and makes delayed decisions due to its large network. This large-scale process may slow flexibility and reaction in a fast-changing banking environment.

7. Digital Transition

Bank of Baroda has progressed toward digitalization but lags faster-growing private-sector banks. The bank must adapt and innovate to fulfill client expectations and stay competitive as technology advances rapidly.

8. Employee Productivity

The bank’s public-sector nature can affect employee productivity, efficiency, and service. These concerns can affect client satisfaction and the bank’s performance, requiring specific personnel motivation and effectiveness measures.

9. Over-reliance on Traditional Banking

Bank of Baroda relies on traditional banking services for revenue. This reliance may hinder the bank’s capacity to capture new growth possibilities and meet changing consumer expectations in an era of FinTech innovation.

10. Aging Infrastructure

The bank’s old branches and systems need significant investment to modernize. Keeping up with technology and modernizing infrastructure improves operational efficiency and customer experience.

11. Regulatory Concerns

The bank has faced various regulatory issues and penalties that could damage its reputation and compliance.

12. Customer Service Issues

Large institutions like the Bank of Baroda often need help to provide consistent customer service across branches and platforms, which can lead to client attrition.

13. Competition

The bank faces fierce competition from public and private banks and NBFCs. This competition forces the bank to innovate, increase efficiency, and improve customer offers to maintain and grow market share.

14. Cybersecurity Concerns

The bank’s growing concentration on digital services raises cyber security concerns. A security breach might damage the bank’s brand and break client trust.

15. HR Challenges

Bank of Baroda must manage a large, diversified workforce, including training, motivation, and retention, to maintain operating efficiency and service quality.

16. Branch Overlap

The merger with Vijaya Bank and Dena Bank caused regional branch overlap and inefficiencies. The bank needs to organize its branch network for coverage and efficiency.

Opportunities for Bank of Baroda

1. Favorable Interest Rate Policies

The RBI has adjusted its monetary policy to balance growth and inflation in response to the strengthening business climate in India. Net interest margins increase for Bank of Baroda (BOB) as interest rates climb.

This could enhance the bank’s interest income minus its interest payments to loans, enhancing profitability. BOB should boost its interest-income-based products now.

2. Increasing Technological Adoption

The digital revolution in India’s financial services presents a huge opportunity for BOB. Online transactions have increased after demonetization and the creation of government-backed platforms like BHIM.

E-transactions are cost-effective and convenient, and the Bank of Baroda may get a high return on technological expenditures by aggressively pushing them.

3. Bancassurance

Banks are increasingly offering insurance products, known as bancassurance. BOB offers IndiaFirst Life Insurance products in a joint venture with Andhra Bank and a UK enterprise. By providing a one-stop financial solution in banking, this strategy could diversify revenue and strengthen customer connections.

4. UPI/Payment Bank

UPI has transformed Indian payment systems. As mobile wallets and UPI-based payment systems like Paytm and PhonePe gain popularity, Bank of Baroda could launch its own UPI Payment app to capture a portion of this boomingmarket and boost customer engagement.

5. Development of Loan Market

BOB might offer competitive loan rates to support infrastructure growth, especially for infrastructure-related firms. By offering attractive loan products, the bank may serve a growing section, boosting national economic development and revenue.

6. Business/Personal Loan Segment

Credit demand for company and personal loans remains constant. Bank of Baroda could increase market penetration and revenue by developing client-centric loan solutions that fit the needs of diverse consumer categories.

7. Digital Banking Expansion

The bank can enhance its internet presence to appeal to tech-savvy customers. Upgrade digital infrastructure, provide user-friendly interfaces, and ensure reliable cybersecurity to support uninterrupted banking services.

8. Rural Banking

Many Indians live in rural areas with minimal financial facilities. By expanding into underbanked communities, BOB may promote financial inclusion and achieve a first-mover advantage in numerous locations.

9. Cross-Selling Opportunities

Bank of Baroda offers many financial goods and services. This allows the bank to cross-sell more products to its existing customers, enhancing client connections and profits.

10. Overseas Expansion

Bank of Baroda might explore international business potential by entering new markets or growing its global presence even in existing locations. This might help the bank reach new customers and diversify earnings.

11. Collaborations and Partnerships

Partnering with fintech, NBFCs, and technology enterprises can lead to innovative banking solutions. Collaborations can boost Bank of Baroda’s products, adding value to clients and keeping it ahead of the competition.

12. Value-Added Services

Investing in wealth management, financial advisory, and financial planning consultancy services can increase bank customer loyalty and profitability.

13. SME and MSME Financing

These sectors are crucial to India’s economy and offer significant lending opportunities. These firms may benefit from Bank of Baroda’s customized services, which could build partnerships and reduce borrowing.

14. Green and Sustainable Banking

Financing renewable energy projects and providing sustainable finance solutions are becoming more popular due to environmental sustainability. Green banking and financing these projects could be crucial for the Bank of Baroda.

15. Customized Banking Solutions

Bank of Baroda can get a competitive edge by creating solutions for certain sectors or consumer segments. These customized services can boost Bank of Baroda’s customer retention and value.

16. Asset Management and Mutual Funds

Indians are increasingly interested in investing in mutual funds and asset management. By entering these areas, BOB may meet the population’s growing investment demand and boost its AUM and fee-based earnings.

17. Government Initiatives

Utilizing government-backed initiatives and plans can significantly boost growth. Bank of Baroda can promote national development goals and grow its client base by supporting the Pradhan Mantri Jan Dhan Yojana and affordable housing.

18. Agri-Finance and Rural Credit

Agriculture is a major economic driver in India. BOB can capitalize on the agri-sector’s huge potential and credit demand by offering customized financial products and services.

19. Innovative Lending Platforms

Bank of Baroda can innovate in lending due to the rise of peer-to-peer and other alternative lending platforms. This can reach more customers and react to changing financing habits.

20. Acquisitions/Mergers

Acquisitions or mergers with smaller banks or financial organizations could help the Bank of Baroda grow strategically. It may easily expand operations, build its customer base, and solidify its market position.

Threats of Bank of Baroda

1. Competition from Private Banks

Private banks with innovative offerings and user-friendly banking experiences compete with Bank of Baroda. These private businesses are more flexible, technologically savvy, and customer-centric, drawing a large clientele seeking ease and modern banking options.

2. Increasing Competition with Foreign Investment

Competition has increased after the Reserve Bank of India allowed foreign banks to invest up to 74% in Indian banks. Bank of Baroda has to innovate to stay competitive and sustain market share due to foreign money in local banks.

3. Rising Non-Performing Assets (NPAs)

Banks struggle with NPAs because they reduce profitability. NPAs can damage Bank of Baroda’s finances and brand, requiring immediate mitigation and recovery strategies.

4. Compliance and Regulation Changes

The banking sector is heavily regulated. Thus, any change in regulatory regulations or compliance norms might disrupt the Bank of Baroda’s operations, requiring costly and time-consuming modifications.

5. Economic Slowdown Impacts

An economic downturn is dangerous. Reduced consumer spending and borrowing capacity lower bank profitability and may increase loan defaults, worsening the NPA problem.

6. Digital disruptions and fintech innovations

The rise of fintech businesses and digital-only banks is changing banking. These competitors can steal clients, especially tech-savvy ones, forcing Bank of Baroda to speed its digital transformation.

7. Cyberthreat

Digitalization, while useful, invites cyberattacks. Cyberattacks and data breaches might damage Bank of Baroda’s reputation, customer trust, and finances.

8. Changing interest rates

Interest rate volatility affects the bank’s loan and deposit product attractiveness and profitability. These shifting rates require robust financial methods to stabilize bank profitability.

9. Operational Risks

Like any major business, the Bank of Baroda faces operational risks from internal process failures or external events that could disrupt its everyday operations.

10. Reputation Risk

A bank’s reputation can be damaged by negative occurrences like financial scams or controversies. A bank with a long history, like the Bank of Baroda, must maintain a clean reputation to stay and gain trust.

11. Geopolitical Tensions

Bank of Baroda works globally thus, geopolitical confusion in any country might hurt its business and financial results.

12. Customer Preference Changes

Modern banking customers, especially younger ones, have changing demands and expectations. Traditional bank services may become less relevant as digital banking and customized services become more popular.

13. Exchange Rate Volatility

Since the bank operates internationally, exchange rate volatility affects its foreign operations, transfer services, and trade finance.

14. Capital Adequacy Pressures

Capital adequacy is essential for regulatory compliance and operational stability. Falling short can force the bank to raise capital, hurting profitability and market perception.

15. Talent Retention Challenges

Keeping talented workers is crucial in a competitive employment environment. Bank of Baroda must attract and retain excellent people to protect its workforce from competition.

16. Rise of New Financial Instruments

Alternative financial platforms and products are altering investment strategies. Traditional banking products must modernize to compete with new offers.

Conclusion

The Bank of Baroda is a worldwide finance giant, combining a historical past with fast modernity. Its large network, diverse service portfolio, and strategic initiatives position it well for today’s banking challenges and opportunities. Despite non-performing assets, operational inefficiencies, and the digital revolution, the bank’s strengths and potential indicate sustainable development and innovation.

Bank of Baroda is prepared to strengthen its history and create new banking excellence by expanding digital frontiers, improving customer service, and adopting global market dynamics. Strategic mergers, digital innovation, and a commitment to financial inclusion show that the bank is forward-thinking and prioritizes trust and customer-centricity.

Liked this post? Check out the complete series on SWOT