Let’s explore the SWOT Analysis of IDBI Bank by understanding its strengths, weaknesses, opportunities, and threats.

A major Indian bank, IDBI Bank has a long history and a creative approach to financial services. IDBI Bank, founded in 1964 to provide loans and other financial services to the expanding Indian industry, has grown greatly. The bank offers retail, business, and international banking using modern technological platforms to improve user experience.

IDBI Bank’s path is distinguished by innovation and customer satisfaction. Strategies and initiatives to empower businesses and individuals reflect its focus on long-term development and financial inclusion. With its solid tradition, powerful infrastructure, and forward-looking vision, IDBI Bank continues to drive India’s economic progress in the digital age.

Overview of IDBI Bank

- Industry: Financial services

- Predecessor: Industrial Development Bank of India

- Founded: 1 July 1964; 59 years ago

- Founder: Government of India (by the IDBI Act, 1964)

- Headquarters: IDBI Tower, WTC Complex, Cuffe Parade, Colaba, Mumbai, Maharashtra, India

- Key people: M. R. Kumar (Chairman), Rakesh Sharma (MD & CEO)

- Revenue: ?30,370 crore (US$3.6 billion) (2024)

- Operating income:?9,774 crore (US$1.2 billion) (2024)

- Net income: ?5,763 crore (US$690 million) (2024)

- Owner: Life Insurance Corporation of India (49.24%), Government of India (45.5%)

- Number of employees: 18,283 (September 2023)

- Capital ratio: 13.31%

- Website: www.idbibank.in

Table of Contents

SWOT analysis of IDBI Bank

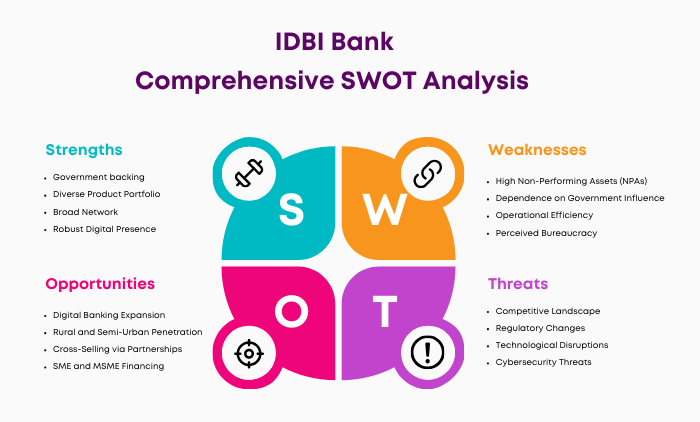

Strengths of IDBI Bank

1. Government backing

IDBI Bank benefits from Indian government backing. This backing gives clients and investors confidence and trust in the bank. In a busy and competitive banking business, the government’s backing helps IDBI stand out and assure stakeholders of its stability and reliability.

2. Diverse Product Portfolio

IDBI Bank specializes in service and product diversity. IDBI offers retail banking, corporate services, and specialized financial support. This diverse portfolio allows the bank to serve customers from simple savings accounts to complex business loans. Its comprehensive strategy retains loyal customers and draws new ones looking for a one-stop banking solution.

3. Broad Network

IDBI Bank has 1890+ branches across India and 3300+ ATMs. This broad reach makes IDBI’s services accessible to many people. IDBI’s presence in cities and villages makes banking easy for millions of Indians.

4. Robust Digital Presence

IDBI supports digitization in today’s fast-paced environment. IDBI has improved client convenience by investing in online and mobile banking options. This digital investment improves customer experience, simplifies operations, and cuts expenses.

5. Legacy and Brand Value

IDBI Bank has a rich legacy dating back to its predecessor entity, the Industrial Development Bank of India, established in 1964 as an apex Development Financial Institution (DFI). Its stable brand attracts customers looking for a reliable bank. IDBI stands out in a competitive and dynamic market with this brand value. As of June 2024, IDBI Bank has a market cap of $11.12 Billion.

6. Experienced Workforce

The bank’s Workforce is its backbone. IDBI’s workers have extensive financial knowledge from years of banking experience. In 2008–09, IDBI Bank had the highest employee productivity among all domestic banks in India, according to a Reserve Bank of India (RBI) report. The experienced team 18,283 can navigate banking operations to provide clients with superior service and creative financial solutions.

7. Financial Inclusion Initiatives

IDBI Bank won the Financial Inclusion and Payment Systems (FIPS) 2013 Award for its Aadhaar Project, which aimed to bring financial inclusion to Direct Benefit Transfer (DBT) districts.

IDBI helps the country’s economy by providing banking and financial services to the poorest. These programs develop an inclusive culture and open new bank markets.

8. Specialised Subsidiaries

IDBI Capital, IDBI Intech, and IDBI Asset Management have expanded the bank’s offerings. These companies allow IDBI to offer more financial services to meet its customers’ needs and promote innovation and growth.

9. NPA Reduction Efforts

NPAs are a major banking issue. IDBI has taken drastic measures to lower its NPA levels, demonstrating its commitment to financial stability. The bank established a dedicated vertical, NPA Management Group (NMG), for focused and aggressive resolution and recovery efforts. IDBI shows durability and forward-thinking through smart recoveries and asset quality improvements.

10. Strategic Alliances

IDBI Bank has increased its product offerings and market reach through partnerships with other institutions and insurance firms. These partnerships allow IDBI to offer customers more services while using its partners’ capabilities and markets.

11. Capacity Building

IDBI prioritizes staff training and development since skilled workers are essential. Such programs keep the bank’s staff current on banking practices and technologies, which are essential for long-term growth and competitiveness.

12. Recent Capital Infusion

IDBI’s equity ratio has improved due to the government’s capital injection. This financial support helps the bank lend more and grow confidently.

13. Adoption of Latest Technologies

Core banking solutions and other new banking technologies help the bank improve customer service and operational efficiency. Modern tech helps IDBI simplify operations, improve data management, and improve customer banking experiences.

14. Risk Management Systems

The dynamic financial sector requires advanced risk management systems. IDBI’s risk management techniques protect it against financial risks, maintaining its long-term stability.

15. Sustainable Banking

IDBI has implemented green banking practices to support global sustainability goals. IDBI’s sustainability activities, from paperless banking to eco-friendly project finance, promote responsible banking and a better future.

Weaknesses of IDBI Bank

1. High Non-Performing Assets (NPAs)

IDBI Bank’s financial performance has suffered from its high NPAs. The bank’s high NPA ratio has hurt its profitability and financial stability. In September 2021, the Reserve Bank of India’s Financial Stability Report found IDBI’s gross NPA ratio at 20.92%, which was worrying.

2. Dependence on Government Influence

Government backing provides stability and security, but IDBI Bank’s excessive reliance on it has rendered it less flexible than its competitors in decision-making. This dependency may hide failing efforts or hinder growth because policy decisions could overpower corporate decisions.

3. Operational Efficiency

IDBI Bank’s operational efficiency lags behind private-sector peers, affecting customer service and satisfaction. The bank’s Cost-to-Net Income Ratio (CIR) as of Q2 FY 2024, the CIR was 47.63%. Continuously high numbers suggest efficiency difficulties and require correction.

4. Perceived Bureaucracy

IDBI Bank, a government entity, faces bureaucracy at multiple levels, which can slow decision-making and execution of new initiatives. The complicated organizational systems and lengthy approval processes can slow innovation and reaction in this fast-paced financial environment.

5. Legacy Systems

IDBI Bank’s old legacy systems can cause compatibility concerns with agile platforms despite efforts to adopt new technology. If technological modernization is delayed, the bank may lose flexibility and effortless user interfaces like most private banks.

6. Employee Morale and HR Challenges

IDBI Bank has suffered labor union conflicts and employee unhappiness over the years, which can produce an undesirable work environment and lower productivity. In September 2019, employees launched a one-day strike over the government’s decision to sell its interest to LIC, raising concerns about the bank’s internal balance sheet.

7. Brand Perception

IDBI Bank is seen as more traditional and less modern than new private banks in several demographics and locations. While this may indicate stability, youngsters prefer banks that prioritize digital change and innovative services.

8. Limited Global Presence

IDBI Bank’s overseas portfolio is weaker than that of its competitors. The bank’s limited global presence limits its opportunity to diversify risk and income streams. Additionally, IDBI Bank struggles to compete with larger private banks regarding market share, innovative product offerings, and customer service. BrandZ found IDBI low on the list of most valuable Indian private banking brands, indicating its competitive position.

10. Cybersecurity Concerns

Like the sector, IDBI Bank risks cyberattacks. Top-tier cybersecurity to protect client data and preserve confidence is an ongoing struggle due to rapid growth in cyber threats.

11. Regulation Challenges

As a government-backed bank, IDBI Bank faces more complex regulations than private banks. These laws can confuse its strategic goals or slow its growth, preventing it from competing with peers.

12. Capital Constraints

Even with periodic government capital treatments, IDBI Bank may have financial constraints that limit its lending and expansion. The RBI’s Prompt Corrective Action (PCA) framework limited the bank’s lending capacity 2019 due to its high NPA and negative RoA.

13. Lag in Technology Adoption

This bank has entered digital banking. However, it may be behind competitors in technical innovation. An S&P Global Market analysis found that FinTech’s adoption and integration of digital technology to improve customer experience has been slower than its competitors, which have entirely adopted digital technologies and are constantly innovating.

Opportunities for IDBI Bank

1. Digital Banking Expansion

Smartphones and persistent internet connectivity have increased digital banking demand. IDBI Bank has an opportunity to improve online and mobile banking. User-friendly features, secure payment options, and comprehensive financial services will help IDBI retain customers and recruit Gen Z and tech-savvy youth.

Since most financial transactions are online, IDBI may lead the banking industry in digital innovation by improving digital banking.

2. Rural and Semi-Urban Penetration

The banking sector has yet to reach a considerable section of India’s rural and semi-urban population. IDBI can expand its banking operations to these locations, a huge opportunity. More branches, ATMs, and mobile banking units can assist IDBI reach new customers and promote financial inclusion and regional economic growth by offering basic to advanced financial services.

3. Cross-Selling via Partnerships

IDBI Bank can cross-sell insurance, mutual funds, and wealth management services through strategic alliances and partnerships. IDBI can offer these new services by utilizing its client relationships, increasing customer satisfaction and loyalty, and expanding revenue streams. This could include cooperating with insurance firms to offer bundled financial products that meet customers’ holistic needs.

4. SME and MSME Financing

The Indian economy relies on the SME and MSME sectors for GDP and employment. These sectors are growing fast yet have trouble getting financing. IDBI Bank may capitalize on this opportunity by offering these enterprises customized loans, credits, and consulting services. This would help SMEs and MSMEs grow, survive, and expand the bank’s loan portfolio.

5. Financial Literacy Initiatives

Financial literacy empowers people to make educated financial decisions and improves financial inclusion. IDBI Bank may host financial literacy classes for students, rural residents, and small business owners. IDBI can develop confidence, expand its customer base, and improve the community’s finances.

6. Sustainable Banking

IDBI Bank can encourage eco-friendly banking practices in response to global sustainability efforts. Offer green financing for sustainable initiatives, paperless banking services, and sustainable investments. IDBI can integrate with global sustainability trends by attracting environmentally concerned clients and businesses as an ecologically responsible bank.

7. NRI Services

The global Indian diaspora demands complete NRI financial services. Money transfers, investment alternatives, and property-related financial services for Non-Resident Indians can be added by IDBI Bank. The bank can increase foreign exchange and investment earnings by serving NRIs.

8. Fintech Collaborations

Fintech pioneers payments, investments, and consumer engagement solutions. IDBI Bank works with fintech companies to use cutting-edge technology and platforms to improve customer experiences, operational efficiency, and product development. Collaborations may encourage innovation in the bank, keeping it competitive in a fast-changing digital world.

9. Asset Reconstruction

IDBI Bank’s NPA record makes it a good candidate for asset reconstruction chances. IDBI can reduce financial risks and boost profits by strategically restructuring and managing troubled assets. It boosts financial recovery and the economy by regenerating failing industries.

10. Value-Added Services

IDBI offers tax advice, investment, and retirement planning beyond typical commercial banking services. IDBI can build customer loyalty and wallet share by establishing a one-stop financial destination. Our services make financial management easier and more comprehensive for customers.

11. Diversification of Portfolio

IDBI Bank should diversify its loan portfolio to reduce market and economic downturn risks. Exploring unexplored sectors and industries allows the bank to spread its risks and find new growth and profit opportunities.

12. Foreign Market Expansion

IDBI Bank might target nations with strong economic ties to India to expand its worldwide presence. IDBI may serve international enterprises and NRI customers by opening branches or forming partnerships in these locations, increasing its worldwide footprint and revenue.

13. Modernizing Physical Infrastructure

Bank branches are changing rapidly. IDBI can attract younger populations who prefer in-person contacts for difficult transactions or consultations by rehabilitating and upgrading its branches. Blending historical values with current aesthetics and technology can make branch visits more appealing and relevant.

14. E-Banking for Businesses

IDBI can improve its business-focused online banking. Strong online cash management, payments, and financial planning capabilities can attract corporate and small company clients seeking efficient and secure individual banking services and solutions.

15. Blockchain and Advanced Technologies

With blockchain technology, IDBI Bank can transform transactions, record-keeping, and data security. Blockchain’s security and transparency make it perfect for fraud prevention, operational efficiency, and consumer confidence. In addition, using AI and ML for predictive analytics, personalized banking, and operational efficiency may establish IDBI as a forward-thinking, innovative bank.

Threats to IDBI Bank

1. Competitive Landscape

Indian banking is a battlefield for IDBI Bank. Established public and commercial banks and dynamic Non-Banking Financial Companies (NBFCs) are all fighting for market share. In this intense rivalry, companies must excel in customer service, product offerings, and technology.

2. Regulatory Changes

Think of banking as a high-stakes game supervised by the regulator. These rules change unexpectedly, causing waves that can disturb IDBI Bank. Stricter laws or unexpected policy changes can increase legal costs and slow the bank’s growth.

3. Technological Disruptions

Technology is transforming financial services. Agility-filled digital upstarts are challenging the old guard. IDBI Bank must evolve or risk extinction. Accepting technological advances is now essential for survival.

4. Cybersecurity Threats

An increasingly connected environment makes cybercrime the modern bandit. Data breaches, hacks, and online fraud cost millions and damage customer trust. As IDBI Bank enters digital waters, cyberattacks become more likely, requiring strong defenses.

5. Economic fluctuations

The economy affects the bank. Economic downturns, interest fluctuation, and inflation can affect loan repayment and profitability levels. Banks like stable financial environments, but they must be ready for economic disturbances.

6. High Non-Performing Assets (NPAs)

Non-performing assets are a banking burden. An increased trend in NPAs may weaken investor trust and financial strength, leaving the bank vulnerable.

7. Reputation Risks

A bank’s reputation is essential in the age of immediate communication. Negative occurrences or perceptions—justified or not—have immediate and far-reaching consequences. Public opinion can greatly reduce IDBI’s reputation and client loyalty.

8. Global Economic Uncertainties

Globalization makes banks like IDBI vulnerable to trade wars and geopolitical unrest. The effects may affect the bank’s foreign operations and financial sector.

9. Customer Preference Change

Modern bank customers are tech-savvy and changing. IDBI Bank must respond to rising customer expectations for fast, transparent, and creative personal banking solutions or risk customer churn.

10. Capital Adequacy Concerns

Reserve Bank of India’s strict bank loss-protection rules are a double-edged sword. IDBI must meet capital adequacy requirements, although profitability variations complicate this.

11. Physical Infrastructure Costs

Digital efficiency competes with financial facilities and marble. An extensive branch network is expensive and may be outdated in the age of mobile and internet banking. IDBI must balance cost and service when streamlining physical presence.

12. Human Resources Challenges

Any technical or organizational change at IDBI will face resistance. Internal and external factors of resistance could stall the bank’s growth unless skills gaps, change motion, and employee morale are addressed.

13. Natural Disasters, Pandemics

As the COVID-19 epidemic showed, invisible enemies strike without notice. Such calamities can disrupt business and cause economic instability, reminding banks to maintain solid contingency plans.

14. Market Share Erosion

Private sector banks’ competitive advantage and aggressive marketing and customer experience strategies threaten IDBI’s market share. Inadequacy is a rival, and differentiation is its friend today.

15. Fraud, malpractice

Internal fraud and unethical actions are murkier. These crimes can cost the bank money and ruin its reputation.

Conclusion

IDBI Bank stands solid in the competitive Indian banking business with its government-backed basis and wide range of financial services. Despite high NPAs and operational inefficiencies, the bank’s digital innovation and client satisfaction position it for success.

Digital banking, rural market development, and fintech collaborations could boost operational efficiency and client reach. IDBI Bank uses its tradition and technology to promote financial inclusion and economic growth in India against competitive constraints and cybersecurity risks.

Liked this post? Check out the complete series on SWOT